Request-to-Pay (RtP) is the new killer app for real-time payments. It is a well-noted fact for banks keen on building a digital future that both real-time payments and open banking should be integral technologies in their respective digital toolboxes. RtP’s are being increasingly deployed as the first overlay services built on top of real-time payment infrastructures.

RtP is a broad term covering many scenarios where a payee initiates a request for a specific payment from the payer. Whilst not considered a new payment type, large rollouts are currently occurring across the globe. They most commonly take the form of a secure messaging service framework that becomes an overlay on top of real-time payment infrastructure. RtP presents a new, more flexible method in which to manage and settle payments between businesses and amongst peers. This is because the details required to make payments – such as the amount, due date and account details – can be messaged directly to the payer.

Banks can benefit from RtP through the creation of new revenue streams and opportunities to better serve customers such as SMEs, as well as from using it as a basis for new ways in which to engage customers. Because RtP solutions offer greater levels of communication, a payee can choose from an array of different responses, each of which would then trigger a different outcome (whether that be a real-time payment or any other types of payment). Within these different outcomes, more advanced responses can be commanded, such as whether to pay the full amount now or at a later date.

Formality vs Functionality

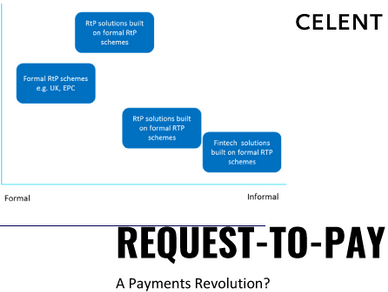

An RtP system can exist in either a formal or informal scheme. The UK’s RtP system is an example of a formal type of payment scheme, with well-defined rules, roles and standards mandated by a scheme coordinator. Others, such as the UPI in India, encourage greater user participation by having the system support multiple use cases that offer great appeal. Informal systems, on the other hand, are those which refer to companies using RtP technology to initiate payments between users of their specific app. Regardless of whether an RtP scheme is formal or informal, it is the customer value and experience, as much as RtP itself, that drives success.

Functionality is also a main aspect of various RtP systems. For example, the UK’s system is currently at the forefront of nationwide schemes in terms of richness of functionality, which co-aligns with its high level of adoption. Informal systems, on the other hand, can feature dynamic QR codes or follow-on apps which can provide a deep level of functionality, but whose focus is rather on time to market and simplicity.

Fundamentals for success

Banks need to consider the different implications that RtP poses to their business. A rise in informal systems may increase the risk of fraud, whereas formal RtP schemes typically employ validation schemes to help reduce this risk. On the other hand, certain informal RtP schemes have excelled at branding themselves, making them well-positioned to replace credit and debit cards.

The “Request-to-Pay: A Payments Revolution?” report analyzes a number of different implications of RtP that banks need to consider:

● Which applications are best for the SME market

● The opportunity to incorporate an end-to-end workflow process

● The ability for larger companies (e.g. utilities) to offer choice of payment options

● Efficiencies of building a technology RtP stack to offer a maximum viable product