As the global payments ecosystem continues to evolve at a rapid pace, it’s once again time to pause and reflect on the current state of payments modernization by way of Volante’s annual “Big Survey”, which aims to serve as a comprehensive overview of emergent capabilities, priorities, and broader modernization trends among banks and financial institutions from around the world.

Garnering 300 full responses from a combination of C-level executives and senior management directors, and building on the insights gained from the previous two years, the results of our 2023 survey convey a continuously growing interest in prioritizing transformation to address a number of increasingly urgent market dynamics. This includes everything from accelerating breakthroughs and customer demands surrounding real-time payments and ISO 20022 standardization, to an increased need for the support of Payments-as-a-Service (PaaS) and cloud-based infrastructure solutions.

In this blog, we’ll explore a few particularly noteworthy insights revealed in this year’s survey, focusing specifically on both confidence in current capabilities, as well as trends in relation to future implementation plans and the utilization of cloud-based payments solutions.

Banks Growing Confident in Strategic Use of Emergent Payment Rails

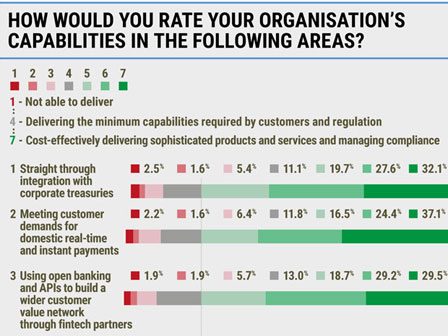

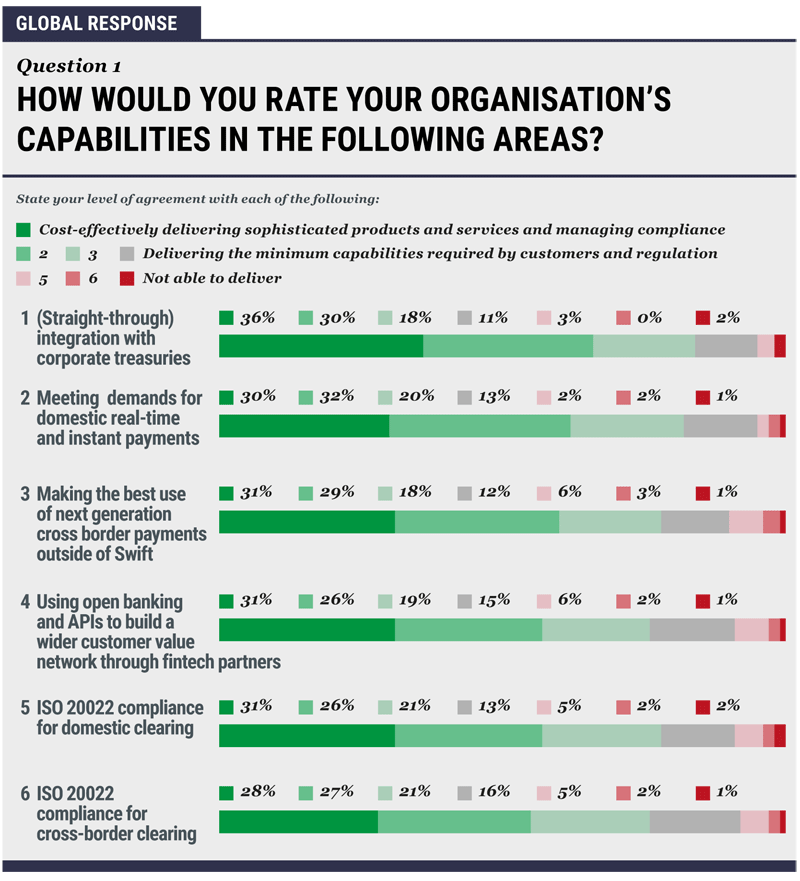

To better understand the current state of capabilities across the global financial sector, we asked our respondents to rate their capabilities in six key areas, ranking each area based on varying degrees of confidence in both cost-effective delivery of services and overall ability to meet compliance requirements (see below).

While the top two answers remained the same from last year (straight-through integration and meeting demands for domestic real-time payments, respectively), with each growing in confidence by a few percentage points, we did find our top third answer to be somewhat of a surprise, and a welcome indicator of banks adopting a more strategic attitude toward modernization as opposed to one primarily concerned with meeting compliance.

More specifically, nearly 80% of respondents expressed confidence in making the best use of next-generation cross-border payments outside of SWIFT, a significant uptick from the 2022 survey, in which this option ranked second to last (out of seven). Beyond highlighting the growing availability and accessibility of emerging networks, this seems to suggest a more focused effort among banks to increase flexibility and cut costs associated with cross-border transactions. In other words, more institutions than ever before are beginning to take a smarter, more strategic approach to determining which rails to use and when, a sign of growing recognition that different networks can be leveraged to achieve more cost-efficient flows on a per-flow basis.

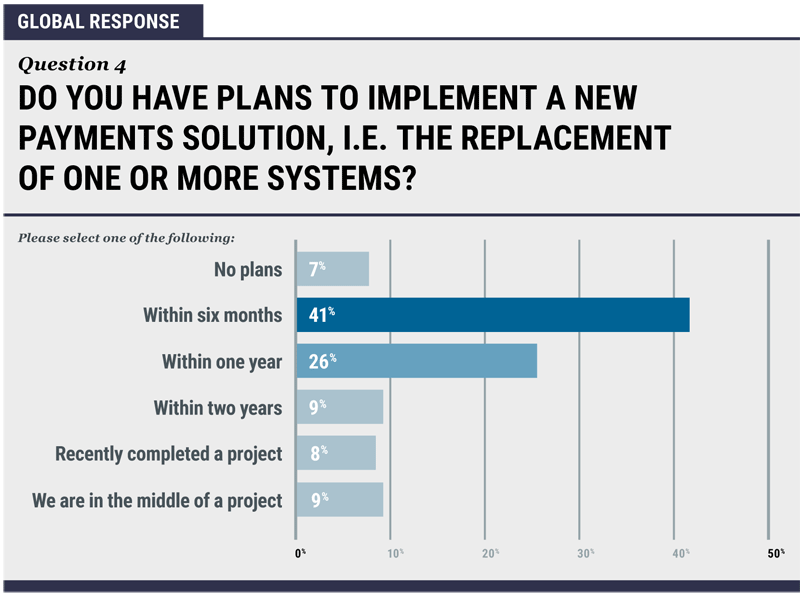

New Implementation Plans Overwhelmingly Feature Cloud-Based Solutions

When asked about plans to implement new payments solutions, not only did the majority of global respondents say they had active plans to replace at least one system, but an impressive 67% expressed confidence that these projects would be underway within a year, including 41% who expected to begin implementation in as little as six months. North American and European banks responded similarly, with 52% and 39% targeting an implementation within the next six months, respectively.

Perhaps even more notable, however, is the fact that a staggering 90% of global respondents said their implementation plans involved the utilization of a cloud-based infrastructure. In North America, this figure was even slightly higher at 91%, which could be indicative of banks in the region seeking out the most agile and cost-effective infrastructure solutions possible in light of the recent launch of the FedNow instant payment service.

More broadly, this finding seems to reflect the growing favorability of cloud-based solutions that have been steadily developing over the years in regard to overall modernization efforts, particularly hybrid and multi-cloud set-ups. Put simply, as financial institutions navigate an increasingly dynamic and at times unpredictable payments environment, they will likely continue to seek out the unique flexibility and overall resilience to change that underpins modern cloud-based strategies.

Banks are Relying on PaaS and Vendor-Provided Solutions More than Ever Before

Finally, perhaps the biggest seismic shift revealed in this year’s survey was the dramatically increased reliance on partners and outside vendors for the implementation of cloud-based infrastructure solutions. More specifically, when asked how cloud-based solutions would be managed, 40% of global respondents said their infrastructure would be handled by a third-party PaaS provider.

This is a nearly fourfold increase (364%) from last year’s result of 11%, and can be viewed as a veritable sea change in reliance on partners throughout the global financial services sector. Once again, this speaks to the growing complexity and accelerating urgency of payments modernization, and suggests that while financial institutions were already up against challenging economic conditions alongside the emergence of new payments rails and standards in 2022, they are now turning to outside vendors in record numbers to help manage and strategically react to the corresponding pressure.

In the next blog, we’ll take a closer look at additional trends surrounding client and market demands and broader drivers behind payments modernization efforts across the global financial landscape. In the meantime, click here to access a complimentary copy of our 2023 survey in its entirety.